Top 5 KYB Onboarding Platforms for Fintech Companies in the US

KYB and KYC Verification

Audit-readiness

If you work in compliance at a fintech, you already know that onboarding a business customer is rarely as simple as confirming a name and an address. You are trying to answer a harder question: is this a real, active company, who actually controls it, and is anyone connected to it on a sanctions list. Getting that wrong is not a small mistake. It can mean a failed exam, a blocked banking partnership, or worse, an account that turns out to be moving illicit money.

That is why so many US fintechs are rethinking how they handle Know Your Business (KYB) onboarding. Manual registry lookups and spreadsheets simply do not scale once volume grows, and regulators on both sides of the Atlantic are paying closer attention to how beneficial ownership is verified and documented.

This guide walks through five KYB onboarding platforms that consistently come up when US fintechs evaluate their options, starting with SpeedyDD, then covering four well established US and Europe headquartered alternatives. We also unpack the regulatory backdrop you actually need to understand in 2026, because the rules around beneficial ownership in the US have shifted more in the last eighteen months than in the previous decade.

What Actually Makes a KYB Onboarding Platform Strong in 2026

Before comparing platforms, it helps to be clear about what good KYB actually requires, because vendors describe their products very differently and it is easy to compare features that are not really comparable.

A genuinely strong KYB onboarding platform for a fintech should cover most of the following.

1) Registry depth. Does the platform pull live data directly from official sources such as Secretary of State offices, the IRS, or international company registries, or does it rely on cached or third party datasets that may be months out of date.

2) Beneficial ownership mapping. Can it identify and verify the individuals who own or control a business, including layered ownership structures, not just the company itself.

3) Sanctions and watchlist screening. Is screening run against entities and against the individuals connected to them, since a clean company name can still hide an individual beneficial owner on a sanctions list.

4) Ongoing monitoring. Onboarding is a single moment, but risk does not stop there. Platforms that support perpetual or continuous KYB, rather than a one time check, are increasingly important given how often ownership and registration status changes.

5) Audit trail and documentation. When an examiner or auditor asks how a business was verified, can the platform produce a complete, reproducible record of what was checked, what was found, and who approved the decision.

How We Approached This Comparison

This list focuses on platforms genuinely used by US fintechs today, based on published product information, documented customer relationships, and how each platform is positioned in the market as of mid 2026. Vendor pricing and feature sets change frequently, so compliance teams should always confirm current capabilities directly with each provider before making a decision. Nothing below is a paid placement. SpeedyDD is included because it is our own platform, and we want to be transparent about that.

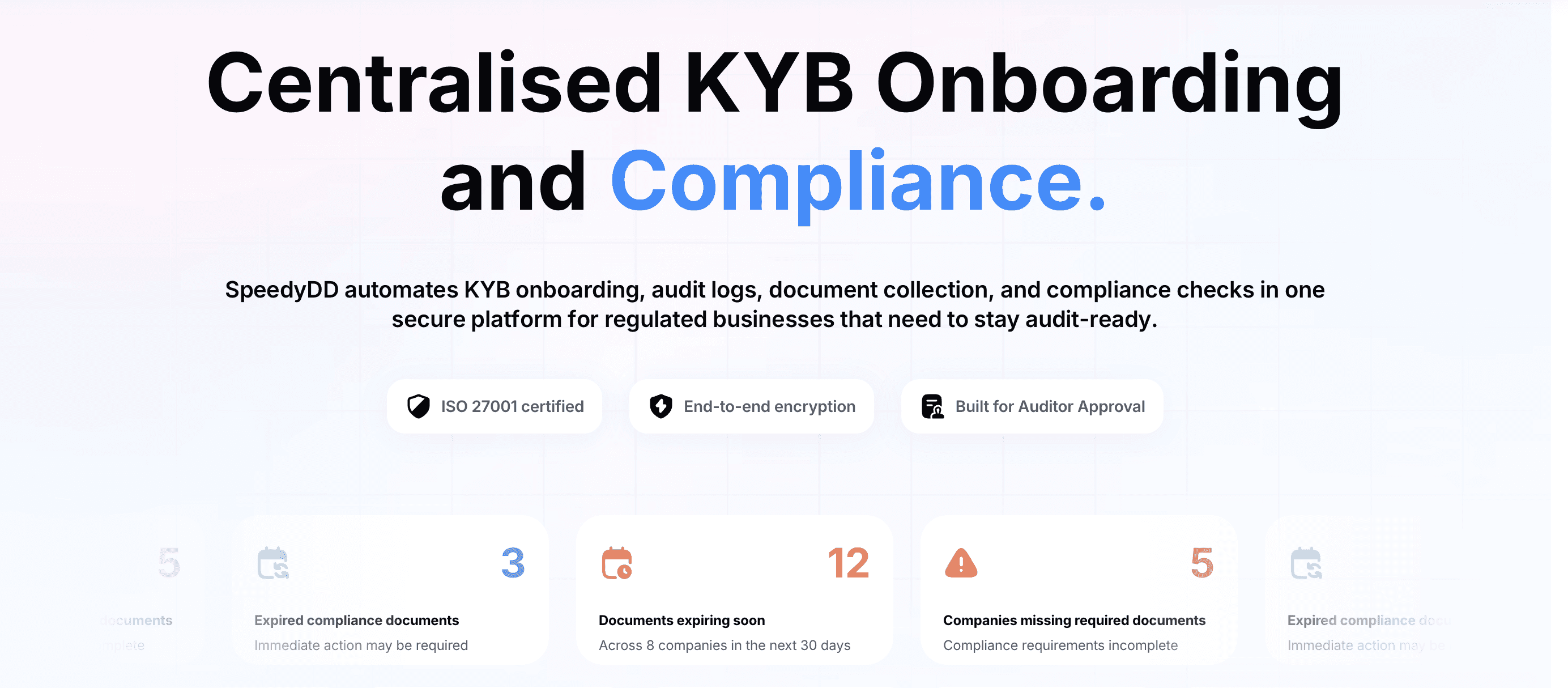

1. SpeedyDD: Best for Audit Ready KYB Onboarding Across Regulated Industries

SpeedyDD is built specifically for the kind of business that cannot afford a sloppy onboarding record: payment service providers, electronic money institutions, corporate service providers, and iGaming operators, alongside fintechs more broadly.

The platform connects to trusted company registries, sanctions lists, and beneficial ownership data sources so verification happens as part of the onboarding flow itself, rather than as a separate manual step bolted on afterward. Company information, registration details, and ownership data are validated as part of onboarding, and every check, decision, and approval is logged automatically. That last point matters more than it sounds. When an auditor or examiner asks how a business customer was verified, the full record already exists rather than needing to be reconstructed after the fact.

SpeedyDD draws on more than 3000 corporate registry data sources across over 200 countries and territories, giving compliance teams reach well beyond US only providers when onboarding international business customers. For cases that need additional verification support, SpeedyDD's marketplace connects teams to more than 230 vetted providers across over 195 jurisdictions, and integrates directly with The KYB for registry data retrieval.

Best for: fintechs, PSPs, EMIs, CSPs, and iGaming operators that need onboarding decisions to be reproducible and audit ready from day one, not just fast.

2. Middesk: Best for Deep US Only Business Verification

Middesk is built specifically for US business verification, and it shows in how deeply it connects to government sources. The platform has direct API connections to Secretary of State offices in all fifty states and Washington DC, plus the IRS, which means it can confirm a business's legal status, registration details, and good standing straight from the primary source rather than a cached snapshot.

According to Middesk, ninety two percent of its business records are updated within ten days, and the platform partners with Socure to extend verification to the individuals associated with a business, supporting beneficial ownership checks alongside the company level data. More than 500 companies reportedly use Middesk, including Plaid, Bluevine, Rippling, and Novo, and the platform has been recognized on Forbes' Fintech 50 list.

The clear limitation is that Middesk's coverage stops at the US border. Fintechs that onboard any meaningful share of international business customers will need a second vendor, or a platform that already covers global registries.

Best for: US focused banks, lenders, and fintechs that primarily onboard domestic businesses and want the deepest possible US registry coverage.

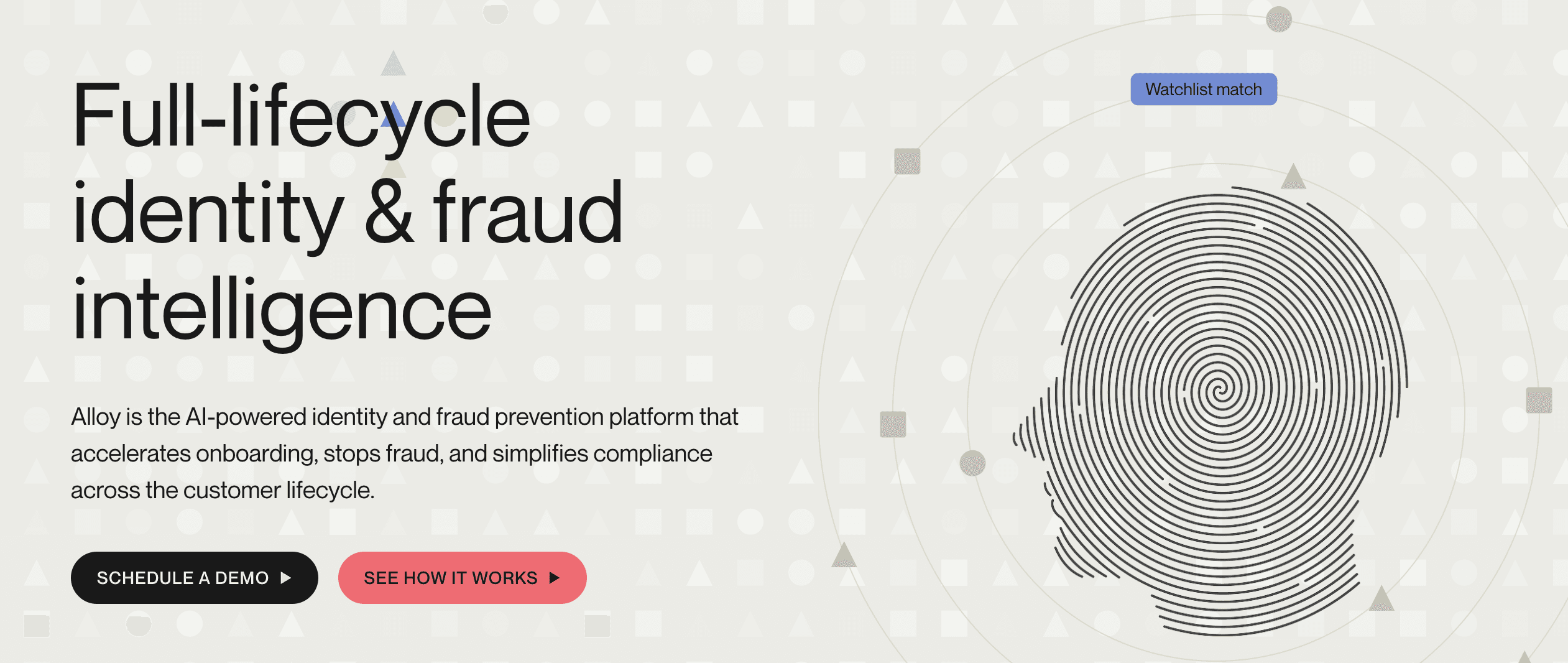

3. Alloy: Best for Configurable Orchestration Across Banks and Fintechs

Alloy, is an orchestration platform that lets compliance teams combine KYC, KYB, AML screening, and fraud signals from more than 200 data sources into one configurable workflow, without needing heavy engineering work to switch vendors or adjust rules.

The company recently extended its perpetual KYB capability into the UK and Europe, reflecting growing demand for continuous, rather than point in time, business monitoring among compliance teams managing cross border risk.

The tradeoff with an orchestration model is that Alloy is not itself the primary data source. Its value comes from how well it lets you combine and configure other providers' data, which is powerful for teams that want flexibility, but means underlying data quality still depends on which sources you connect.

Best for: banks, credit unions, and fintechs that want a single configurable workflow across KYC, KYB, AML, and fraud, and have the internal resources to set up the rules properly.

4. Trulioo: Best for Global Reach Alongside US Coverage

Trulioo, supports verification across hundreds of millions of business records and billions of individual identity records spanning roughly 195 countries, and it has been used by major institutions including JPMorgan Chase, Mastercard, and Airwallex.

For US fintechs whose roadmap includes international expansion, Trulioo's appeal is that you are not adding a second vendor every time you enter a new market. The platform combines KYC and KYB verification in a single workflow and uses AI and natural language processing to normalize data that arrives in different languages and formats from different countries.

The honest caveat, echoed across multiple independent reviews of the KYB data provider space, is that Trulioo's depth in some European commercial registries is not as granular as dedicated regional registry providers, so teams with heavy European business onboarding volume may want to pair it with a registry specialist.

Best for: US fintechs that need one platform covering both domestic and international business and individual verification as they expand.

5. Sumsub: Best Europe Headquartered All in One KYC, KYB, and AML Platform

Sumsub, founded in 2015 and headquartered in London, is the platform most often mentioned when crypto exchanges and fintechs talk about needing KYC, KYB, and AML screening in one dashboard rather than three separate tools. According to Sumsub, the platform supports verification across more than 220 countries and includes AML screening natively within the same workflow used for onboarding.

When registry data is not available for a given jurisdiction, Sumsub maintains an in house compliance team that manually reviews corporate documents from more than 140 countries, which is a meaningful fallback for fintechs onboarding businesses from smaller or less digitized markets. Reported clients include crypto and fintech platforms such as Bybit, Bitpanda, and TransferGo.

One detail worth flagging for budget planning is that Sumsub's pricing model is reportedly based on completed checks, including rejected ones, so fintechs with a higher onboarding rejection rate should model costs carefully rather than assuming a flat per approved customer rate.

Best for: fintechs and crypto platforms, particularly those with European ties, that want KYC, KYB, and AML unified in a single vendor relationship.

Comparing the Five Platforms at a Glance

Platform | Headquarters | Strongest Fit | Watch For |

|---|---|---|---|

SpeedyDD | Cyprus, EU | Regulated industries needing audit ready, reproducible KYB records & Compliance document management | U.S. EU, EMEA coverage. |

Middesk | San Francisco, US | Deep, direct US Secretary of State and IRS data | US only coverage |

Alloy | New York, US | Configurable orchestration across KYC, KYB, AML, and fraud | Data quality depends on connected sources |

Trulioo | Vancouver, Canada | Combined global KYC and KYB in one workflow | Thinner depth in some European registries |

Sumsub | London, UK | Unified KYC, KYB, and AML for fintech and crypto | Per check pricing can add up with high rejection rates |

The US Regulatory Backdrop Compliance Teams Need to Track in 2026

Choosing a KYB platform is only half the job. The regulatory ground underneath US beneficial ownership rules has moved substantially since early 2025, and any platform you choose needs to be flexible enough to keep up.

The Corporate Transparency Act's beneficial ownership reporting requirement, administered by the Financial Crimes Enforcement Network, originally required most US companies to report their beneficial owners directly to FinCEN. That changed in March 2025, when FinCEN issued an interim final rule that exempted all domestic reporting companies and their beneficial owners from that requirement, narrowing the obligation to apply only to foreign companies registered to do business in the United States. As of mid 2026, FinCEN has not yet finalized that interim rule, and the underlying legal questions remain active, including a December 2025 appellate ruling that upheld the Corporate Transparency Act's constitutionality. Compliance teams should treat this as an evolving area rather than a settled one, and should not assume the domestic exemption is permanent.

It is worth being precise here, because this is one of the most commonly confused points in fintech compliance right now. The Corporate Transparency Act's domestic exemption applies to reporting beneficial ownership directly to FinCEN. It does not remove a separate, longstanding requirement that covered financial institutions identify and verify the beneficial owners of their own legal entity customers under FinCEN's Customer Due Diligence Rule. That rule still requires institutions to identify anyone who owns 25 percent or more of a legal entity customer, plus one individual with significant managerial control, at the time a new account is opened.

There was a meaningful update to how that rule works in practice in February 2026, when FinCEN issued an order granting covered financial institutions exceptive relief from re verifying beneficial owners at every single new account opening. Institutions can now rely on previously collected beneficial ownership information, provided the customer certifies it remains accurate, rather than repeating full verification each time. This shifts the practical emphasis toward platforms that support ongoing, risk based monitoring rather than only point in time checks at onboarding, which is exactly the kind of capability several platforms on this list, including SpeedyDD, Alloy, and Sumsub, are actively building toward.

Sanctions screening remains a separate but closely related obligation. The Treasury's Office of Foreign Assets Control expects financial institutions to maintain a risk based sanctions compliance program, and its own compliance framework guidance is a useful baseline for understanding what examiners look for when they review how a fintech screens both entities and the individuals connected to them.

For fintechs headquartered in the EU, or US fintechs with EU subsidiaries, it is worth keeping an eye on the EU's own overhaul of its anti money laundering rules. The new EU Anti Money Laundering Regulation becomes directly applicable across all member states from 10 July 2027, replacing the old directive based system with a single harmonized rulebook, including a standardized 25 percent beneficial ownership threshold and oversight from the newly established Anti Money Laundering Authority based in Frankfurt. Any fintech operating on both sides of the Atlantic will want a KYB platform that can flex between US and EU beneficial ownership definitions without rebuilding workflows from scratch.

How to Actually Choose Between These Platforms

There is no single best answer here, because the right platform depends heavily on where your business customers actually come from and how your team is set up.

If your business is almost entirely US domestic and you want the deepest possible registry data, Middesk's direct government connections are hard to beat, but plan for a second vendor if international onboarding becomes part of the roadmap. If you want one configurable workflow that spans fraud, KYC, KYB, and AML, and your team has the capacity to build out the rules, Alloy's orchestration model gives you the most flexibility. If global reach matters from day one, Trulioo and Sumsub both offer broad coverage, with Sumsub leaning toward fintech and crypto use cases and Trulioo leaning toward enterprise scale institutions. And if audit readiness, reproducible documentation, and support across PSPs, EMIs, CSPs, and iGaming operators are central to how your business is regulated, that is exactly the gap SpeedyDD was built to close.

Whichever platform you choose, run a real pilot before committing. Test it against your actual customer mix, including the harder cases, layered ownership structures, less digitized jurisdictions, and any high risk sectors you serve, rather than relying only on a vendor's demo environment.

Final Thoughts

KYB onboarding is not getting simpler in 2026. Beneficial ownership rules in the US are still in flux, the EU's new AML framework is coming into force on the other side of the Atlantic, and fraud techniques targeting business onboarding are getting more sophisticated. The platforms compared here all solve real pieces of that problem, but the right choice comes down to your customer base, your team's capacity, and how seriously your business needs to take audit readiness, not just onboarding speed.

About SpeedyDD

SpeedyDD exists because regulated businesses, payment service providers, EMIs, CSPs, iGaming operators, and the fintechs that serve them, should not have to choose between fast onboarding and a clean audit trail. Our mission is to help complex, regulated companies stay audit ready by default, connecting KYB checks, UBO mapping, sanctions screening, and document verification into a single workflow with every decision logged automatically. SpeedyDD is built for compliance teams who need to prove, not just promise, that their onboarding decisions hold up under scrutiny.

Frequently Asked Questions

What is the difference between KYB and KYC?

KYC verifies an individual person's identity. KYB verifies a business entity, including its registration status, legal structure, and the individuals who own or control it. Most KYB processes include a KYC component, since you ultimately need to verify the human beneficial owners behind the company.

Is KYB legally required for US fintechs?

It depends on what the fintech does and which regulator oversees it. Banks and other covered financial institutions are required under FinCEN's Customer Due Diligence Rule to identify and verify the beneficial owners of legal entity customers when opening new accounts. Many fintechs operate through bank partnerships, and the underlying bank's regulatory obligations often flow through to how the fintech must structure its own onboarding and due diligence processes.

Does the Corporate Transparency Act change what fintechs need to do for KYB?

Not directly. The Corporate Transparency Act's beneficial ownership reporting requirement governs what companies report to FinCEN about themselves. It does not replace a financial institution's separate obligation under the Customer Due Diligence Rule to identify and verify the beneficial owners of its own legal entity customers during onboarding.

How often should a business customer's KYB information be refreshed?

There is no single fixed schedule mandated for all institutions. FinCEN's February 2026 exceptive relief order allows covered financial institutions to rely on previously verified beneficial ownership information, provided it is periodically certified as accurate, rather than re verifying it at every new account opening. Beyond that, most compliance programs use a risk based schedule, refreshing higher risk customers more frequently than lower risk ones, and triggering an immediate refresh whenever ownership or control changes are detected.

What ownership threshold counts as a beneficial owner?

In the US, FinCEN's Customer Due Diligence Rule generally defines a beneficial owner as anyone who owns 25 percent or more of a legal entity customer's equity, plus a single individual with significant managerial responsibility. The EU's new Anti Money Laundering Regulation harmonizes a similar 25 percent threshold across member states, though it allows the threshold to be lowered to 15 percent for higher risk sectors.

Do crypto and payments platforms need a different level of KYB scrutiny?

Generally yes, in practice if not always in strict legal threshold. Crypto exchanges, payment service providers, and other higher risk verticals typically face closer regulatory and banking partner scrutiny, which is why several platforms on this list, including Sumsub and SpeedyDD, have built specific workflows and manual review fallbacks for jurisdictions and business types that carry elevated risk.

Can a single KYB platform handle both US and international business verification?

Some can, though depth varies by region. Trulioo and Sumsub both combine US and international coverage in one workflow, and SpeedyDD's registry network spans more than 200 countries and territories. Middesk, by contrast, is intentionally US only, so fintechs with international ambitions will need to pair it with a global provider or choose a platform built for global coverage from the start.

How much does a KYB onboarding platform typically cost?

Pricing varies widely and most providers do not publish rates publicly, since cost depends on verification volume, jurisdiction mix, and whether ongoing monitoring is included. Some platforms price per completed check regardless of outcome, which can meaningfully change the total cost for fintechs with higher onboarding rejection rates, so it is worth asking any vendor directly how their pricing model handles rejected or incomplete checks.